By Topic

CSL Limited (ASX: CSL) – Structural Quality Re-Asserted

We believe CSL Limited (ASX: CSL) remains one of the highest-quality global healthcare franchises listed on the ASX, with FY25 marking a clear re-acceleration in earnings quality, cash flow conversion, and strategic clarity. While the share price has periodically struggled to reflect this underlying strength, we view CSL as misunderstood rather than mis-executing.

3 ASX Stocks on Solid Share Price Uptrends

Every so often, the market serves up a handful of charts that practically nudge you to take a closer look. You know the type, steady higher lows, clean breakouts, and that subtle shift in momentum that hints at a story unfolding beneath the surface. In this piece, we’re turning the spotlight on three ASX-listed stocks whose price action has been speaking in a clear and confident tone. These aren’t wild speculative swings or one-off spikes; they’re structured uptrends that have earned their place on watchlists through consistent behaviour.

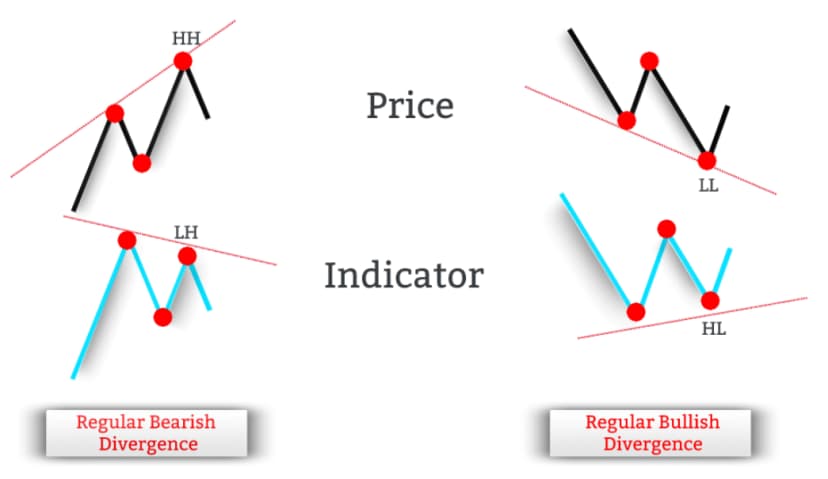

3 ASX stocks with confirmed bullish divergence patterns

The Australian share market has a habit of sending quiet signals before a move actually happens. One of the most reliable of those signals is bullish divergence, a moment when price looks weak, but momentum quietly starts to improve. In this article, we’ll take a closer look at three stocks listed on the (ASX) that are currently showing confirmed bullish divergence patterns.

Megaport Limited (ASX: MP1), Re-Establishing Structural Growth Leverage

Megaport has evolved from a cash-intensive growth story into a more disciplined, cash-generative digital infrastructure business, with FY25 marking a clear structural turning point as costs reset, churn stabilised and balance-sheet risk reduced. While the market still views the company through outdated perceptions, we see improved unit economics, renewed credibility and emerging operating leverage, positioning Megaport for growing free cash flow and ongoing relevance in an increasingly hybrid, multi-cloud world.

Xero Limited (ASX: XRO): From Accounting Software to Global Small Business Operating System

Xero is transitioning from a high-growth SaaS accounting platform into a global small business operating system with improving earnings quality and rising operating leverage. FY26 interim results show resilient revenue growth, margin expansion from cost discipline, and deeper monetisation across payments, payroll and financial services. We believe the market still applies an outdated growth-at-any-cost lens, underestimating Xero’s emerging cash generation and embedded optionality.

Why is SportsHero's (ASX: SHO) share price rising and how much higher can it go?

SportsHero (ASX: SHO) is an early-stage Australian sports gamification and media company focused on mobile-first prediction and gaming platforms across Southeast Asia, primarily Indonesia. It offers leveraged exposure to regional digital gaming growth but carries high execution, funding and profitability risk typical of small-cap platform build-outs.

...